How to Report Sick Pay, Tips, and Adjustments on Form 941

reading time: 13 minute(s)

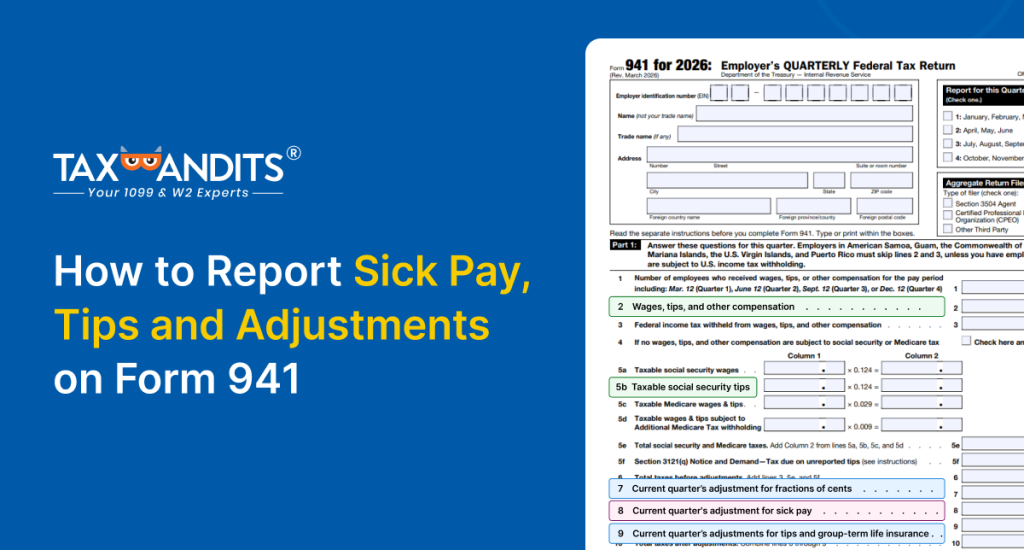

Form 941, the Employer’s Quarterly Federal Tax Return, is filed by most employers to report wages, federal income tax withheld, and Social Security and Medicare taxes. While the basics are straightforward, three areas often cause confusion: third-party sick pay, employee tips, and tax adjustments.

Getting these right matters. Errors in these fields can lead to miscalculated tax liability or IRS notices.

Reporting third-party sick pay

Third-party sick pay refers to payments made to your employees by a third party, typically an insurance carrier, during periods when employees the unable to work due to illness or injury.

Who reports what? The responsibility depends on the agreement between the employer and the third party:

- If the third party withholds and deposits the taxes, they report it on their own Form 941

- If the employer takes on that responsibility, it must be included in the employer’s Form 941

Where does it go on Form 941? Third-party sick pay is reported on Line 8 as a negative adjustment, which prevents the amount from being double-counted because the third party has already handled the tax deposits.

Reporting employee tips

Employees who receive tips must report them to their employer, and employers are responsible for including that tip income on Form 941.

Two types of tips to know:

- Reported tips — Tips employees report to you directly. These are included in Box 1 of the W-2 and factor into Social Security and Medicare tax calculations

- Allocated tips — Tips assigned to employees when their reported tips fall below 8% of gross receipts. These appear on the W-2 but are not included on Form 941

Where do tips go on Form 941?

- Line 5b — Reports Social Security taxes on reported tips

- Line 5c — Reports Medicare taxes on reported tips

One thing to note: If your business is in the food and beverage industry and has 10 or more employees on a typical business day, you’re likely required to file Form 8027 annually to reconcile tip income; this works alongside your Form 941 reporting.

Adjustments on Form 941

Adjustments on Form 941 exist to account for small discrepancies and specific situations that affect your total tax liability. There are three key adjustments employers need to be aware of:

- Fractions of Cents (Line 7) – When calculating Social Security and Medicare taxes, rounding across multiple employees can create minor differences between what was withheld and what was deposited. Line 7 is where you correct those small rounding gaps, typically just a few cents.

- Sick Pay Adjustment (Line 8) – As covered earlier, this is where third-party sick pay is entered as a negative figure to avoid double-counting taxes already handled by the insurance carrier.

- Tips and Group-Term Life Insurance (Line 9) – Uncollected Social Security and Medicare taxes on tips and employer-provided group-term life insurance over $50,000 are reported here.

Why do these adjustments matter? Skipping them, even if the amounts seem small, can cause a mismatch between your tax liability and your deposits, which may trigger an IRS notice.

Common mistakes to avoid

Even with a good understanding of Form 941, these are the errors that come up most often:

- Confusing Employer vs. Third-Party Responsibility for Sick Pay – Not clarifying upfront who handles the tax deposits on sick pay can lead to either double-reporting or missing it entirely. Always confirm the arrangement with your insurance carrier before filing.

- Not Reconciling Tip Income Properly – Mixing up reported tips and allocated tips is a common slip. Remember—allocated tips don’t belong on Form 941. Only tips actually reported by employees factor into your Social Security and Medicare tax calculations.

- Skipping Adjustments – Many employers skip Lines 7, 8, and 9, assuming they don’t apply. But even a minor fraction-of-cents difference left unreported can create a mismatch between your liability and deposits—putting you on the IRS’s radar unnecessarily.

- Missing the Filing Deadline – Form 941 is due by the last day of the month following each quarter. Late filing, even with correct numbers, can result in penalties.

Conclusion

Reporting third-party sick pay, employee tips, and adjustments on Form 941 doesn’t have to be complicated—but it does require attention to detail. Each of these elements has a specific place on the form and clear rules around who reports what.

To recap:

- Sick pay from a third party goes on Line 8 as a negative adjustment

- Reported tips factor into Lines 5b and 5c—allocated tips do not

- Adjustments on Lines 7, 8, and 9 keep your liability and deposits aligned

When in doubt, consult a payroll professional or refer to the IRS instructions for Form 941 before submitting. A few minutes of double-checking can save you from a costly correction later.

If you’re looking to simplify the process further, TaxBandits can help you e-file Form 941 accurately, reduce manual errors, and stay compliant with federal requirements—so you can focus less on calculations and more on running your business.

Leave a Comment