The IRS Released Draft Form 941-X for 2026: Things to Know Before Filing 941 Corrections

reading time: 10 minute(s)

If you’ve ever had to correct a previously filed Form 941, you already know it’s not a “fix it and forget it” situation. Every correction leaves a paper trail — and the IRS pays close attention to how (and why) you make those changes.

That’s exactly why the draft Form 941-X for the 2026 tax year matters more than it sounds. Let’s walk through what’s new

Looking for the latest Form 941 for 2026 updates?

Refer to our detailed article covering the key changes, what’s new, and what employers need to know.

Form 941-X in 2026: What’s New This Year?

Here’s a quick overview of the most important updates employers should be aware of.

1. New Withholding Rules for Tips & Overtime

One of the most significant updates comes from P.L. 119-21, also known as the One Big Beautiful Bill Act.

For tax years after 2024 and before 2029, employees and certain workers can now claim new deductions on their individual income tax returns:

- Up to $25,000 for qualified tips

- Up to $12,500 for qualified overtime pay

- $25,000 if married filing jointly

Employer Impact

Employees may submit an updated Form W-4 to adjust their federal income tax withholding to account for these expected deductions. Employers must:

- Use the employee’s most recent Form W-4

- Follow the federal income tax withholding procedures in Publication 15-T

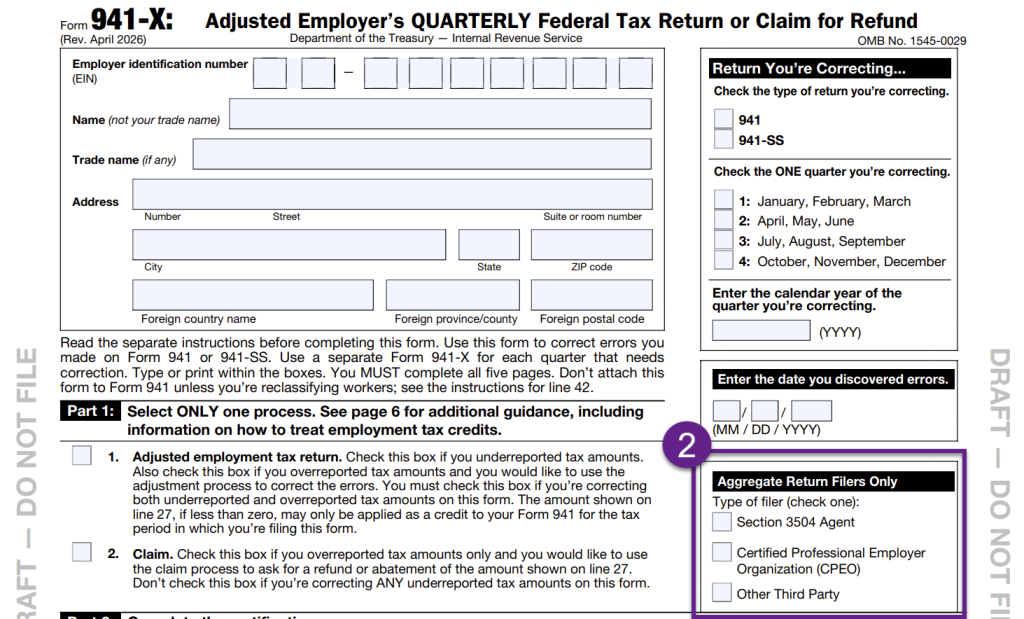

2. New Section for Aggregate Return Filers

The draft Form 941-X now includes a new “Aggregate Return Filers Only” section. This applies to third parties who file employment tax returns on behalf of others, such as:

- Section 3504 agents

- Certified Professional Employer Organizations (CPEOs)

- Other authorized third-party filers

These filers must now clearly identify their role when submitting a corrected aggregate return. In some cases, they may also need to attach Schedule R (Form 941). This change improves IRS tracking and accountability for payroll reported through third parties.

3. Major Limits on Employee Retention Credit (ERC) Corrections

There’s also an important update related to the COVID-19 Employee Retention Credit (ERC).

Under the new law:

- ERC claims for Q3 and Q4 of 2021 are no longer allowed

- Refunds or credits for those quarters are only valid if the claim was filed on or before January 31, 2024

Extended Audit Period

The IRS now has more time to assess ERC claims for those quarters:

- The assessment period is extended to 6 years

- Employers should keep ERC-related records for at least 7 years

If you’re considering filing a 941-X related to ERC for the late 2021 quarters, this change is especially important.

Why These Draft Changes Matter Now

Even though this is still a draft form, it sends a clear signal about where IRS enforcement and reporting expectations are headed.

Understanding these updates now helps you:

- Avoid trying to correct federal withholding errors that aren’t allowed.

- Prepare for employee W-4 updates related to tip and overtime deductions.

- Stay compliant if payroll is filed through a third party.

- You cannot file ERC corrections that are no longer permitted.

Maintain proper documentation for extended IRS review periods

Final Thoughts

Think of the 2026 draft Form 941-X updates as your early heads-up from the IRS. The rules around payroll tax corrections are becoming clearer, tighter, and more structured — especially when it comes to withholding adjustments and ERC claims.

The takeaway is simple: the more you know now, the smoother things will be later. Staying informed, keeping solid records, and understanding what can and can’t be corrected will help you handle payroll fixes with confidence — and avoid surprises you definitely don’t want.

Leave a Comment