Form 941 for 2026 Released: Key Changes Employers Should Know

reading time: 20 minute(s)

Form 941, also known as the Employer’s Quarterly Federal Tax Return, is used by employers to report wages paid, federal income tax withheld, and employment taxes to the Internal Revenue Service.

The IRS has released the final version of Form 941 for 2026. While it closely resembles the Q1 2025 version, there are some important changes that employers should be aware of.

This blog provides a clear breakdown of the updates the IRS has made to the 2026 Form 941. Let’s take a closer look.

Key Changes in Form 941 for 2026

Here are the 5 key changes the IRS has made to Form 941 for 2026:

1. Updated Social Security Tax Rates and Wage Threshold

- Increase in Social Security Wage Base Limit: For 2026, the Social Security wage base limit has increased to $184,500. Wages above this threshold are not subject to Social Security tax withholding.

- Adjusted Threshold for Household Workers: Social Security and Medicare taxes will apply to cash wages of $3,000 or more paid to household workers in 2026.

- Adjusted Threshold for Election Workers: Election workers earning $2,500 or more in cash or equivalent compensation in 2026 will be subject to Social Security and Medicare taxes.

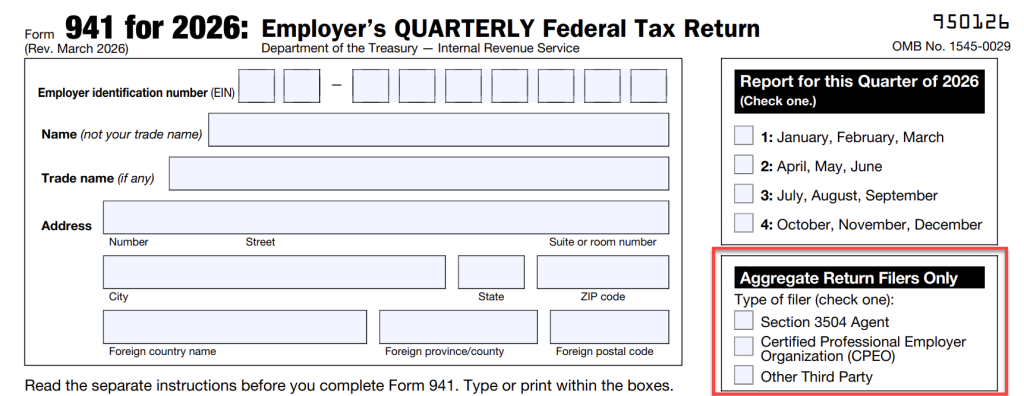

2. New Checkbox Added for Aggregate Filers

The 2026 Form 941 introduces a new checkbox section specifically for aggregate filers. This applies to authorized aggregate filers who file Form 941 on behalf of multiple employers, allowing them to clearly indicate their aggregate filing status.

This section applies to:

- Section 3504 Agents

- Certified Professional Employer Organizations (CPEOs)

- Other third-party filers

What to do if you select the aggregate filer checkbox

If you select this checkbox, you must also complete and attach Schedule R (Form 941), Allocation Schedule for Aggregate Form 941 Filers, along with your Form 941 filing.

3. Direct Deposit Refund Option Added to Form 941 Line 15

The IRS has introduced new fields on Form 941 for 2026 that allow employers to receive refunds of overpayments through direct deposit. To support this change, Line 15 has been expanded into multiple fields (Line 15a–15e) where employers can provide their bank account information when requesting a refund.

This update aligns with the federal government’s initiative to modernize payment systems under Executive Order 14247 – Modernizing Payments to and From America’s Bank Account, which directs federal agencies to transition toward electronic payments for both government disbursements and payments made to the government.

As a result:

- Employers must also make payroll tax payments electronically using electronic funds transfer (EFT) through systems such as EFTPS, IRS Direct Pay, or an IRS Business Tax Account.

- Refunds issued by the IRS are moving toward electronic delivery through direct deposit, replacing paper checks.

- Line 15a – Overpayment:

This field shows the total amount overpaid for the quarter. - Line 15b – Choose your option:

Select how to handle the overpayment. You can choose to:- Apply it to your next return, or

- Request a refund

- Line 15(c) – Routing number:

If you’re requesting a refund, you can now enter your bank’s routing number to receive the amount by direct deposit. - Line 15(d) – Type of account:

Indicate whether the type of bank account is checking or savings. - Line 15(e) – Account number:

Enter the actual account number where the refund should be deposited.

In previous Form 941, overpayments were often issued by check, which could delay the refund process. With the updated Form 941 for 2026, employers can now opt for direct deposit refunds, making the process faster and more secure.

4. Form 941 Return Transcripts Now Available Electronically

For tax years 2023 and later, Form 941 return transcripts are now available electronically via your IRS Business Tax Account. Employers can use this feature to verify filings and reconcile payroll reporting efficiently.

5. Withholding on Qualified Tips and Overtime Compensation

Under P.L. 119-21 (One Big Beautiful Bill Act), the IRS provides updated rules for withholding and reporting on qualified tips and overtime compensation

- Qualified Tips: Employees can deduct up to $25,000 of cash tips for 2025–2028. Employers must withhold federal income tax using updated W-4s, while Social Security and Medicare taxes still apply.

- Qualified Overtime: Employees may deduct up to $12,500 ($25,000 if married filing jointly) of overtime pay above their regular rate. Social Security and Medicare taxes still apply.

- Reporting: Employers must report tips and overtime on W-2s or 1099s and provide statements to recipients. Transition relief is available for 2025 reporting.

Next Step: Learn How to File Form 941 for 2026!

Now that you understand the latest Form 941 changes for 2026, the next step is ensuring accurate and timely filing. Learn how to file, key deadlines, and available e-filing options for employers.

A Quick Summary of the Changes in 941 Form 2026

| Changes | Current Version (2026) | Previous Version (2025) |

| Aggregate Filer Identification | New section to check if filer is a Section 3504 Agent, CPEO, or Other Third Party | Not included |

| Refunds via Direct Deposit | Expanded 15a and 15e to collect bank details for direct deposit | Basic options: apply to the next return or request a refund |

| Social Security / Medicare | The Social Security and Medicare tax rate remains unchanged Social Security Wage base: $184,500 | Standard rates (Social Security 6.2%, and Medicare 1.45%) Social Security Wage base: 176,100 |

| Qualified Tips Deduction | Deduction up to $25,000; adjust withholding via W-4 | Not included |

| Qualified Overtime Deduction | Deduction up to $12,500 ($25,000 MFJ); report via W-2/1099 | Not included |

| Electronic Payments & Transcripts | EO 14247 mandates electronic payments; transcripts are available online | Not included |

What Should Employers Do Now?

With the final version of Form 941 for 2026 released by the Internal Revenue Service, employers should take the following steps to ensure accurate and compliant 941 filing:

- Review your filing status: If you act as an aggregate filer, determine whether you are filing as a Section 3504 Agent, CPEO, or other third party. You may be required to indicate your filing status on Form 941.

- Plan for refund handling: If you expect overpayments, consider how you’ll provide banking details for faster refunds via direct deposit, especially if you manage multiple returns.

- Maintain accurate payroll records: Keep detailed and organized records of employee wages, federal income tax withheld, and employment taxes. This helps ensure accurate reporting and simplifies reconciliation if needed.

- Prepare for timely filing: Use the correct 2026 version of Form 941 when filing your quarterly Form 941 to avoid rejection, processing delays, or potential penalties.

The Bottom Line

The release of 941 Form 2026 reflects the Internal Revenue Service’s continued efforts to improve payroll tax reporting accuracy and transparency. While the overall structure of Form 941 remains familiar, employers should pay close attention to the updates, ensure payroll records are accurate, and file Form 941 using the IRS-recommended electronic filing method.

Employers who choose to file Form 941 electronically can use an IRS-authorized e-file provider such as TaxBandits. Electronic filing helps ensure faster processing, improved accuracy, and immediate confirmation once the return is accepted by the IRS.

Article Sources:

- Internal Revenue Service. “About Form 941, Employer’s Quarterly Federal Tax Return“.

- Internal Revenue Service. “Form 941: Employer’s Quarterly Federal Tax Return“.

- Internal Revenue Service. “Instructions for Form 941“.

Leave a Comment