reading time: 15 minute(s)

The IRS has released the draft version of Form W-2 for tax year 2026 (filed in 2027). While draft forms are not final, they offer valuable insight into upcoming compliance requirements.

Whether you’re handling payroll, overseeing year-end reporting, or managing compliance, this early look at the changes under the One Big Beautiful Bill Act (OBBBA) is your opportunity to stay ahead of the curve.

What’s new in Form W-2 for 2026?

One of the biggest changes in the 2026 Form W-2 is the increase in the wage reporting threshold, but this is not the only update—several other reporting and compliance changes have been introduced that employers need to be aware of.

1. Wage reporting threshold increased

For wages paid after calendar year 2025, the threshold for filing Form W-2 has been updated. Under the new 2026 rules:

- The wage reporting threshold increases from $600 to $2,000.

- This $2,000 threshold applies only if NO federal income tax, Social Security tax, or Medicare tax was withheld.

- If any federal tax is withheld, employers must file a Form W-2 regardless of the total wages.

The IRS has indicated that this $2,000 threshold will be adjusted annually for inflation starting after 2026.

2. State paid family and medical leave (PFML) reporting

The updated form includes guidance for reporting Paid Family and Medical Leave (PFML) programs.

According to the IRS instructions, both employee and employer contributions to PFML must be included as wages on Form W-2.

The IRS specifically references Revenue Ruling 2025-4 and Notice 2026-6, which provide additional guidance on the wage treatment of PFML contributions.

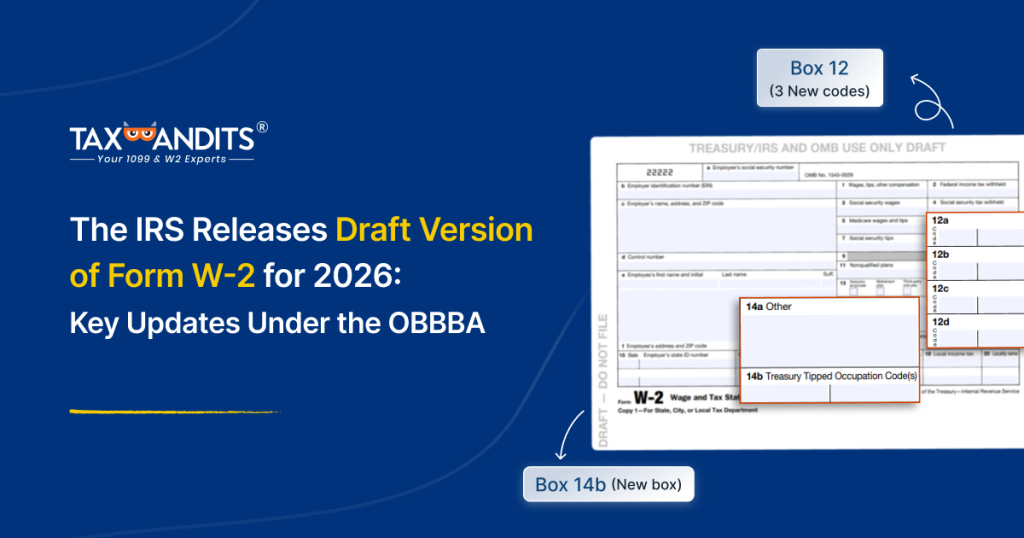

3. Box 14 updates: Introduction of Box 14a and Box 14b

The IRS has revised Box 14 on Form W-2 by dividing it into two separate fields. This change applies to Forms W-2, W-2AS, W-2GU, W-2VI, and W-2c.

- Box 14a: Other

Employers will use Box 14a to report information that was previously reported in Box 14, including state disability insurance taxes withheld, union dues, uniform payments, employee-paid health insurance premiums, nontaxable income, and educational assistance payments. - Box 14b: Treasury Tipped Occupation Codes

Box 14b is a newly introduced field used to report up to two Treasury Tipped Occupation Codes for an employee whose occupation involves tipped income.

4. Box 12 Updates

Several new codes will be used to report deductions and employer contributions.

These changes apply to tax years beginning after 2024 and ending before 2029 and affect how certain types of income and contributions must be reported to the IRS and furnished to employees.

- Code TP: Reporting deduction for qualified tips

Box 12, Code TP is used to report the total amount of cash tips reported by an employee to the employer. Certain employees and self-employed individuals may deduct up to $25,000 of qualified tips on their income tax return, subject to IRS eligibility rules. What are qualified tips?

- Code TT: Reporting qualified overtime compensation

Box 12, Code TT is used to report qualified overtime compensation. Individuals (employees and others not treated as employees) may deduct up to $12,500 of qualified overtime ($25,000 if married filing jointly) on their federal income tax return. What is qualified overtime compensation? - Code TA: Employer contributions to Trump accounts

Box 12, Code TA will be used to report employer contributions to Trump accounts for employees or their dependents. What are Trump accounts?

Employers may contribute up to $2,500 per year toward the employee’s or dependent’s Trump account, which is part of the $5,000 annual contribution limit (excluding certain exempt contributions).

After tax year 2027, the contribution limits will be adjusted for inflation.

Penalty updates

The IRS has increased the maximum penalties for failure to file, failure to furnish, and for intentional disregard of W-2 filing and payee statement requirements. These adjustments reflect inflation-based updates and apply to returns required to be filed after December 31, 2026.

| Filing Situation | 2025 | 2026 |

| File within 30 days after the due date | $60 per W-2 Maximum: $683,000 ($239,000 for small business) | $60 per W-2 Maximum: $698,500 ($244,500 for small business) |

| File more than 30 days after the due date, but by August 1 | $130 per W-2 Maximum: $2,049,000 ($683,000 for small business) | $130 per W-2 Maximum: $2,095,500 ($698,500 for small business) |

| File after August 1, fail to file corrections, or do not file required W-2s | $340 per W-2 Maximum: $4,098,500 ($1,366,000 for small business) | $340 per W-2 Maximum: $4,191,500 ($1,397,000 for small business) |

Other important reminders for employers

Beyond the primary 2026 updates, employers should be aware of several ongoing compliance requirements to avoid errors and penalties. These reminders reflect key areas that continue to impact wage reporting and employee statements.

- Health FSA Limits: The 2026 limit for Health Flexible Spending Accounts (FSA) is $3,400 per employee.

- Medicaid Waiver Payments: Certain Medicaid waiver payments can be excluded from gross income and reported in Box 12 using Code II.

- EITC Notices: Employers must provide Earned Income Tax Credit (EITC) notices to eligible employees.

The bottom line

By reviewing these updates now, you give yourself time to adjust payroll systems, refine internal processes, and communicate effectively with employees. While the draft form is not final, it offers valuable guidance that can help you stay ahead of compliance requirements and avoid surprises when the 2026 filing season arrives.

Now that the 2025 tax year filing season is in full swing, file your W-2s efficiently with TaxBandits.

Leave a Comment