The Latest IRS Guidance For Payroll Tax Credits Related To COVID-19

reading time: 10 minute(s)

It is not often that the IRS creates completely new tax forms or extends the deadlines for IRS reporting, however the COVID-19 pandemic has caused huge changes to every aspect of our lives. In these unprecedented times, many small businesses are struggling to adapt and remain solvent amid the current economic crisis.

As of March 31, 2020, the IRS has begun to release additional guidance on the payroll tax credits that employers can request an advance of. You may not have the time to review pages of IRS literature, who does? So, here are the high points that you will need to know to successfully request these credits and take advantage of the relief that your business needs.

What are Employee Retention Credits?

Understanding Employee Retention Credits is crucial. These credits are designed to encourage employers to keep their entire staff on payroll by limiting the financial burden of doing so.

Under the CARES Act, employers with 500 employees or less that are fully operational during the 2020 calendar year are eligible for Employee Retention Credits on up to 50% of qualified wages. These credits apply to the employer’s portion of social security taxes and $10,000 is the limit that can be applied to any one employee in the span of a calendar year.

It is important to note that if your business has received an economic impact loan, it is no longer eligible for the Employee Retention Credits.

What are FFCRA Credits?

These credits refer to the Families First Coronavirus Response Act. This Act mandates that all employers must provide their full-time employees with two weeks of paid sick leave if they or a member of their family suffer from COVID-19. Under the FFCRA, employers can receive tax credits to cover the cost of these wages.

What is the IRS Guidance for these Credits?

Let’s cover the latest IRS guidance related to these tax credits. This is another topic that employers are finding particularly confusing, and with good reason! The IRS has released guidance in Notice 2020-22 to lay out the proper protocol for tax credits, it contains 8 pages of information. Again, let’s cover the highlights that you actually need to know.

You may be worried about claiming these tax credits and the possibility of incurring IRS penalties. Don’t worry, the IRS has set up guidelines to address this concern. Employers are able to reduce their employment tax deposits in anticipation of both the FFCRA credits and the Employee Retention Credits without fear of penalties.

When it comes to reporting/requesting an advance on these tax credits from the IRS there are two key IRS Tax Forms to keep in mind. The Form 7200 and the Form 941. As your business already files the Form 941, the Employer’s Quarterly Federal Tax Return, you will already be familiar with it. This form will be updated to accommodate these changes for the second quarter of 2020 and we can expect this to be released in the near future.

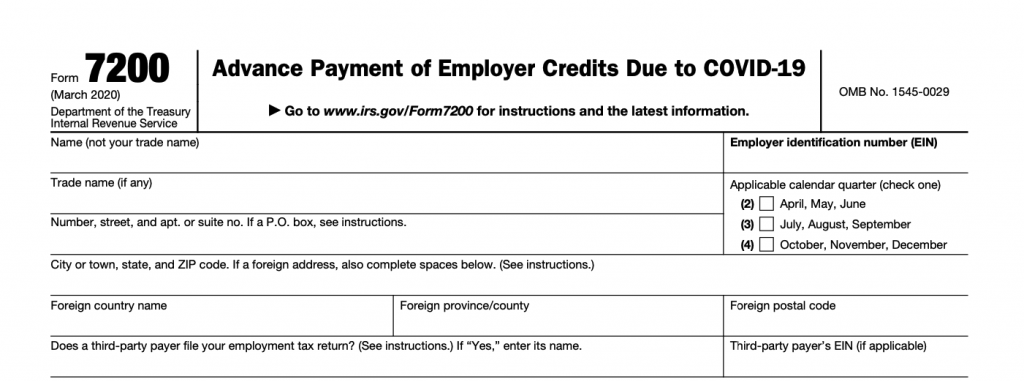

What is the Form 7200?

This is a completely new IRS Tax Form that you may have heard about. The Form 7200 was designed by the IRS to give employers the opportunity to claim an advance payment of excess social security tax credits. This form reports the following credits…

- Employee Retention Credits

- Paid qualified sick leave

- Paid qualified family leave

This form can be filed multiple times throughout each quarter as needed.

How do I File Form 7200?

You’re in luck, TaxBandits is here to help you complete the Form 7200. We have added it to our line up of IRS Tax Forms to help your business speed up the tax relief process. Just enter the required information and our software will help you calculate the amount you are eligible to request. Then, we will handle the IRS submission of your Form.

For more information on filing the Form 7200 with TaxBandits check out this video!

Leave a Comment