A Comprehensive Guide to Form 1099-QA: Understanding Distributions from ABLE Accounts

reading time: 19 minute(s)

Imagine the peace of mind that comes with having a financial safety net, especially for individuals managing disabilities. ABLE (Achieving a Better Life Experience) accounts provide that very safety net, enabling individuals to save for future expenses without losing access to vital government benefits. While ABLE accounts offer many advantages, the process of reporting distributions can seem overwhelming. But don’t worry—Form 1099-QA makes it simpler than you might think.

In one of our previous blog posts, we shared the exciting news that TaxBandits now supports e-filing for Form 1099-QA and Form 1098-F, making compliance with IRS regulations easier than ever. In this blog, we’ll focus specifically on Form 1099-QA, explaining its purpose, who needs to file it, and the essential filing requirements to ensure a smooth and compliant process.

Let’s dive into everything you need to know about Form 1099-QA and how it plays a crucial role in ABLE account distributions.

What is an ABLE Account?

Before we dive into the specifics of Form 1099-QA, it’s important to understand the ABLE account itself. Established under the Achieving a Better Life Experience (ABLE) Act of 2014, ABLE accounts are tax-advantaged savings accounts designed to help individuals with disabilities manage their financial needs without losing eligibility for critical government benefits like Medicaid and SSI.

These accounts can cover a variety of qualified disability expenses, including housing, education, healthcare, and more. The contribution limits for ABLE accounts are $18,000 for 2024 and $19,000 for 2025, offering individuals with disabilities the opportunity to build a secure financial future. To be eligible for an ABLE account, an individual must:

- Be blind or disabled before age 26.

- Be both the owner and the designated beneficiary of the account.

- Only have one ABLE account at a time.

Now that we have a clear understanding of ABLE accounts let’s see how Form 1099-QA comes into play.

What is Form 1099-QA?

Form 1099-QA, titled “Distributions From ABLE Accounts,” is an essential information return that reports any distributions made from ABLE accounts during the calendar year. This form ensures that both the IRS and the designated beneficiary are aware of the amounts withdrawn from the account and that they comply with the rules governing these accounts.

The information reported on Form 1099-QA is vital for maintaining the tax-advantaged status of ABLE accounts. Whether you’re a state agency administering an ABLE program or a tax professional assisting a beneficiary, understanding how and when to file this form is crucial to ensuring compliance with IRS regulations.

Who Must File Form 1099-QA?

The responsibility for filing Form 1099-QA lies with the entity managing the ABLE program. This typically includes:

- Any state, state agency, or instrumentality that administers a qualified ABLE program.

- The responsible entity must file Form 1099-QA for each ABLE account that had distributions or was terminated during the calendar year.

- An authorized officer, employee, or designated representative of the state or agency overseeing the ABLE program is responsible for ensuring accurate filing.

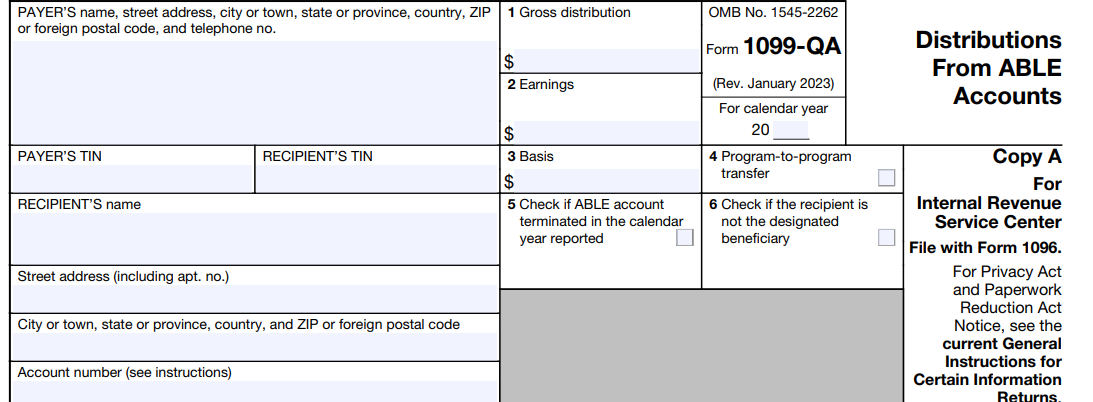

What Information is Reported on Form 1099-QA?

To complete Form 1099-QA, you will need the following information:

- Payer Information: Name, address, and TIN of the state or other applicable agency managing the ABLE account.

- Recipient Information: Name, address, and TIN of the designated beneficiary (ABLE account holder).

- ABLE Account Distribution Information: Let’s break down the information to be reported in each box of Form 1099-QA.

- Box 1 (Gross Distribution): The gross distribution from the ABLE account refers to the total amount of money withdrawn or distributed from the account during the calendar year. This total includes any amounts the designated beneficiary plans to roll over into another ABLE account. However, it’s important to note that gross distribution does not include program-to-program transfers.

- Box 2 (Earnings): The earnings portion of the total amount withdrawn from the ABLE account (Box 1). Earnings refer to the growth in the account, such as interest, dividends, or investment gains. To calculate this amount, follow the regulations section 1.529A-3(c) guidelines, which outline how earnings are determined when distributions are made.

- Box 3 (Basis): Report the distribution amount that represents the return on investment in the ABLE account. To find this amount, the following formula is used,

Basis (Box 3)=Gross Distribution (Box 1)−Earnings (Box 2) - Box 4 (Program-to-Program Transfer Checkbox): Check this box if funds were directly transferred from this ABLE account to another ABLE account during the year. It involves the direct transfer of the entire balance from one ABLE account to another of the same designated beneficiary. Program-to-program transfers differ from rollovers and should be reported separately.

- Box 5 (ABLE Account Terminated Checkbox): Mark this box if the ABLE account was terminated during the calendar year.

- Box 6 (Other Than Designated Beneficiary Checkbox): Check this box if the distribution reported on the 1099-QA form has been made to someone other than the designated beneficiary of the ABLE account.

- Box 1 (Gross Distribution): The gross distribution from the ABLE account refers to the total amount of money withdrawn or distributed from the account during the calendar year. This total includes any amounts the designated beneficiary plans to roll over into another ABLE account. However, it’s important to note that gross distribution does not include program-to-program transfers.

| Example: If the ABLE account had an excess contribution (money deposited above the allowed limit) and that money is being returned to the contributor instead of the designated beneficiary, then check Box 6. |

When is Form 1099-QA Due?

It’s important to know the deadlines for submitting Form 1099-QA to avoid penalties. Here are the key dates:

- The deadline to e-file 1099-QA with the IRS is March 31st.

- The deadline to furnish recipient copies of the 1099-QA form is January 31st.

Make sure to meet these deadlines to ensure compliance with IRS regulations.

What are the Penalties for not Filing Form 1099-QA?

According to section 6693, the penalty for failing to file Form 1099-QA with the IRS on time is $50 per return with no maximum limit.

| Section 6693 Section 6693 pertains to penalties for failing to provide required reports on certain tax-favored accounts or annuities. This penalty applies to the following IRS forms, such as 1099-SA, 5498-SA, 5498, 1099-Q,1099-QA, 5498-QA, and 5498-ESA. Learn more about the 1099 Penalties in detail here |

What’s the Process for Requesting an Extension to File 1099-QA?

To request an extension for filing or furnishing recipient copies of Form 1099-QA, the following IRS extension forms can be used:

- Form 8809: If accepted, this form grants an extension of 30 days to file Form 1099-QA with the IRS.

- Form 15397: If accepted, this form grants an extension of 30 days to furnish copies of Form 1099-QA to recipients.

Ensure these forms are filed by the original due date to qualify for the extension.

Simplify Your 1099-QA E-filing with TaxBandits!

TaxBandits makes your Form 1099-QA filing easier than ever. Our intuitive software offers time-saving features such as data import and validation for error checks, seamless recipient copy distribution, advanced security, and world-class customer support.

Click here to learn more about how TaxBandits simplifies the 1099-QA filing process.

Ready to File Form 1099-QA?

Leave a Comment