Drafts of Form 943, 944 and 940 are Now Available with COVID-19 Changes

reading time: 15 minute(s)

The IRS has released a historic number of revised tax forms this year due to the COVID-19 pandemic. The IRS has rolled out new drafts of several employment tax returns that are filed on an annual basis, including the Form 943, 944, and 940.

As an employer you are busy adapting to the constantly changing economic environment that this pandemic has produced, so your annual tax forms may be the last thing on your mind. To ease the stress of figuring out these new drafts and how your reporting will change this year, TaxBandits is breaking them down for you!

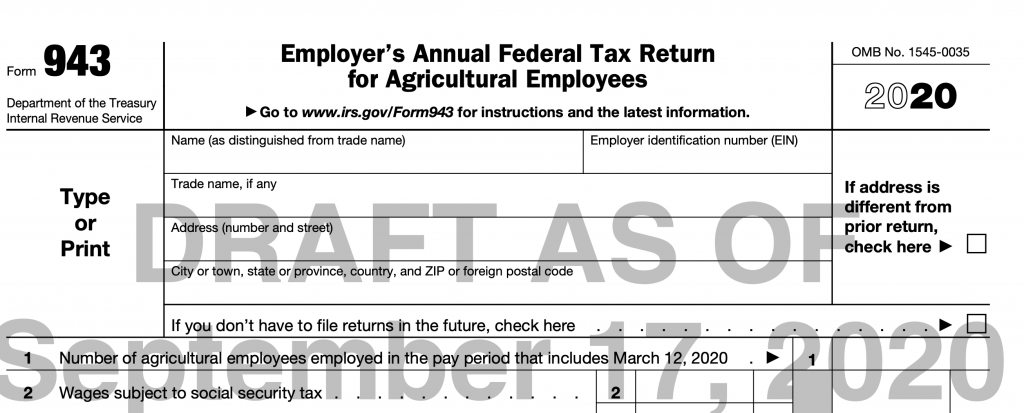

Form 943

The Form 943, Employer’s Annual Federal Return for Agricultural Employees, is just this: an annual form that employers in the agricultural industry file with the IRS each year.

Changes to Form 943

The changes to Form 943 are reflective of the changes made to the quarterly Form 941 regarding COVID-19 tax credits. These are the lines that have been either added or affected:

- Lines 2a and 2b now refer to the qualified family and sick leave wages.

- Line 3a and 3b will now be used to report the total social security taxes including the social security taxes related to qualified sick and family leave wages.

- Lines 12a, 12b, 12c, and 12d report the following:

- 12a- Qualified small business payroll tax credit for increasing research activities

- 12b- Non Refundable portion of credit for qualified sick and family leave wages

- 12c- Non Refundable portion of employee retention credit from Worksheet 1

- 12-d Total nonrefundable credits (this line requires that you add together the amounts from 12a, 12b, and 12c)

- Line 13 refers to the total taxes after adjustments and nonrefundable credits, (to find this amount you will need to subtract Line 12d from Line 11.

- Line 14 has been broken up into lines 14a, 14b, 14c, 14d, 14e, 14f, 14g, and 14h, these lines are now used to report the following:

- 14a- total deposits for 2020, include any overpayment applied from a previous year/ Form 943-X

- 14b- Deferred amount of the employer share of social security tax

- 14c- Deferred amount of the employee share of social security tax

- 14d- Refundable portion of the credits for qualified sick and family leave wages

- 14e- Refundable portion of the employee retention credit from Worksheet 1

- 14f- Total deposits, deferrals, and refundable credits (To get this amount you will need to add up the previous lines starting with 14a)

- 14g- Total advances received from filing Form 7200

- 14h- Total deposits, deferrals, and refundable credits less advances. Subtract line 14g from 14f

- Lines 18 and 19 refer to both the qualified health plan expenses from sick leave and family leave wages.

- Line 20 and 21 reports the qualified wages for the employee retention credit and related health plan expenses.

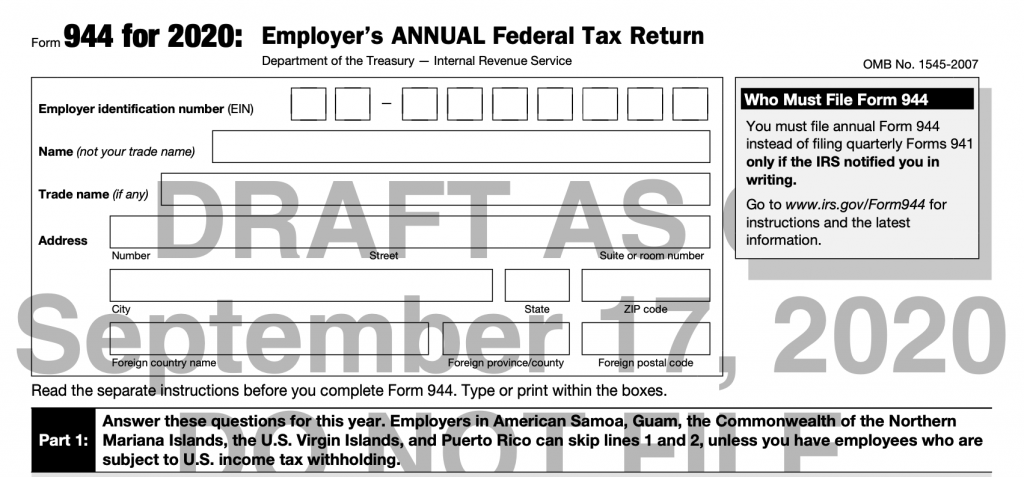

Form 944

Form 944 is the Employer’s Annual Federal Tax Return. This form is filed by employers annually in place of the Form 941, which is a quarterly form. This form can only be filed by employers that have written permission from the IRS.

Changes to Form 944

The following lines of the Form 944 have been either added or affected due to the COVID-19 tax credits:

- Lines 4a(i) and 4a(ii) reference the qualified sick and family leave wages.

- Lines 8b, 8c, and 8d refer to nonrefundable tax credits

- Line 8b- Non refundable portion of credit for qualified sick and family leave wages

- Line 8c- Non refundable portion of employee retention credits

- Line 8d- Total non refundable credits, this line is the sum of 8a, 8b, and 8c.

- Line 10a refers to the total tax deposits for the year, including overpayments.

- Line 10b and 10c report the deferred amounts of both employer and employee shares of Social Security.

- Lines 10d and 10e report the tax credits that are refundable, including qualified family and sick leave wages and the employee retention credit.

- Line 10f is the sum of all deposits, deferrals, and refundable credits.

- Line 10g should be used to report the amounts received by filing Form(s) 7200 throughout the year.

- Line 10h reports the total deposits, deferrals, and refundable credits minus the advances, you will need to subtract Line 10g from 10f.

- Lines 15 and 16 should be used to report the qualified health plan expenses from family and sick leave.

- Line 17 reports the qualified wages from the employee retention credit.

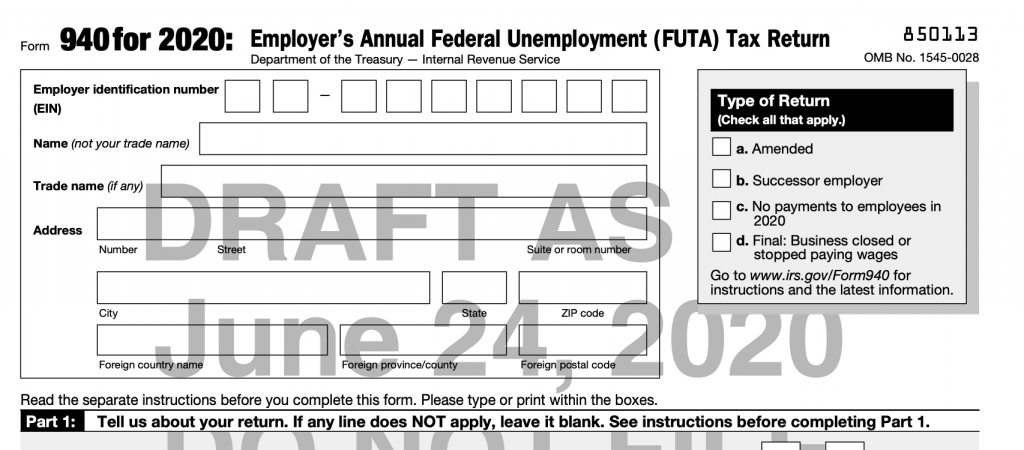

Form 940

This is the Employer’s Annual Federal Tax Return. This form is filed annually by employers to report their Federal Unemployment Tax Act or FUTA taxes. This must be filed by all employers that paid $1500 or more in employee wages throughout the calendar year.

Unlike the other two annual forms, the Form 940 doesn’t contain a considerable amount of changes due to COVID-19. This form is however updated for tax year 2020.

There is also a draft of Form 940 Schedule A available for 2020.

File all these Forms and more with TaxBandits!

That’s right! If you need an e-filing solution for any of these annual forms, look no further than TaxBandits. We offer a simple e-filing solution for Form 943, 944, and Form 940.

As the IRS continues to roll out changes for tax year 2020, we are here to help you adapt to these changes and prepare for your deadlines. Remember, these forms that the IRS has released are just drafts, they are never meant to be filed with the IRS. We may see additional changes in the finalized versions.

As soon as the IRS finalizes these forms, our application will be updated and ready so that you can file your form easily and accurately with the IRS. Create a free TaxBandits account to get started today!

Leave a Comment